Can You Roll a 401k Into Sep Ira

One big goal on Financial Samurai is to highlight to readers what is financially possible. Once you know what is possible, you minimize your limiting beliefs and tend to strive much farther. You can actually save more than $100,000 in your pre-tax retirement accounts per year! Let me explain with some basics first.

The 401k maximum contribution for 2021 is $19,500. The increases will likely continue by $500 increments every year or two to keep up with inflation. Contributing the maximum pre-tax a year for 30+ years will most likely make you a 401k millionaire by the time you retire.

Unfortunately, $3 million is the new $1 million, and in 30 years, $7 million will likely be the new $1 million if we assume a 3% annual inflation rate!

The 401k is not enough for most people to retire on. Sure, we potentially have Social Security to help us when we reach, at the earliest, 62 years of age. But I wouldn't count on the government to properly manage our money until then. Beyond maxing out a 401k every year, I encourage everyone to also invest at least 20% of their after-tax, after-401k money into a diversified investment portfolio.

As a contractor over the past year, I've discovered something that will really supercharge one's pre-tax retirement savings. The discovery still seems too good to be true, but it is true. The research I've done is based off the IRS website, my own experience, and speaking to Fidelity's small business retirement department where I have a rollover IRA, SEP-IRA, and Solo 401k.

How To Save Big In Your Pre-Tax Retirement Savings Plans

Let's say you've got a cushy job paying $212,000 a year. You contribute $19,500 to your 401k and get a nice 4% match.

Furthermore, you can contribute to a traditional IRA because you make too much. Therefore, what is a retirement super saver supposed to do if s/he wants to save more than $19,500?

Answers:

1) Find a better employer who will contribute more to your pre-tax retirement savings account(s). $57,000 max 401k contribution for 2021 (employer profit sharing + $19,500 by employee)

or

2) Be an employee and a contractor/business owner! Max is $114,000.

The first thing I did when I left my old job of 11 years was roll over my 401k into an IRA. There are many benefits to a rollover IRA, including more investment options and lower costs.

The only issue with my rollover IRA is that I can no longer contribute pre-tax to the investment account. Its growth mainly comes from asset and dividend growth. I don't bother contributing $5,500 in after-tax money because of the two other retirement accounts I get to contribute pre-tax.

As an employee of an online media company, I get to participate in the company's SEP-IRA plan. Any self-employed individual or business owner with or without employees can open up a SEP-IRA. The funds are completely funded by the employer.

The employer can contribute up to 25% of compensation, up to a maximum of $57,000 in 2021. Doing simple math to discover how much income you need in order to save $57,000 using a 25% contribution rate = $57,000 / 25% = $228,000. IRS link on SEP.

Making $228,000 is not exactly a piece of cake as an employee. You've probably got to pay your dues over many years to get to such a level or more, but it's possible.

If you do manage to make $228,000 in income, you've still got to pay Federal tax, State tax (if you are not living in a no income tax state), and FICA tax (6.2% Social Security + 1.45%) on that income. After you make $228,000 or more, you've got to then convince your employer to contribute 25% of your income to your SEP-IRA.

As an independent contractor, I've opened a Solo 401k (aka KEOGH 401k, Self-Employed 401k, One-Participant 401k), which is meant for a business owner with no employees.

My duties as an employee for an online media business is different from my contracting business. The online business makes money mainly through advertisement. My contracting business makes money by me consulting with other companies mainly on their content marketing initiatives.

The Solo 401K has the same contribution limits of up to 25% of compensation, to a maximum of $57,000. So in other words, I can try and make $228,000 as an independent contractor to contribute $57,000 pre-tax in my Solo 401k as well.

The grand result is that a ~$440,000 combined income can ultimately save a total $114,000 in retirement accounts tax deferred. The combined adjusted gross income (AGI) is therefore $440,000 – $114,000 = $326,000, which is taxed at a 35% marginal Federal tax bracket.

I originally thought the total pre-tax retirement contribution was $57,000 across all accounts. But when I called the Fidelity retirement department for small businesses, they verified with me that I can indeed contribute $114,000 total if I have two separate accounts as an employee (with no ownership) and independent contractor.

The idea is to open a SEP-IRA as an independent contractor/business owner if your employer has a 401k program, and vice versa. If you open up a solo 401k while already contributing to an employer 401k, then the max you can contribute is $57,000 combined.

The Ideal Retirement Income / Savings Scenario

Given there is a progressive tax system in America (see chart), making $500,000 a year in combined income might not be the best move to avoid the marriage tax penalty, which has almost all but gone away after Trump's 2018 Tax Reform plan.

If you decide that you want to make $500,000 a year in income to contribute ~$120,000 in pre-tax retirement money, then you must make $500,000 as an employee and as a contractor/business owner.

Remember, there's only one type of main retirement account per business entity, and that one retirement account limit is $57,000 a year or 25% of income, whichever is less. In other words, if you make $425,000 in your business alone, you can't contribute $425,000 X 25% = $108,000. You can only contribute $54,000 to your SEP.

The solution is to therefore try and earn as close as possible to $220,000 in income as an employee for the SEP-IRA, and another $212,000 as an independent contractor for your Solo 401k.

Pay Attention To Government Policies

Remember, the government sets these pre-tax contribution rules, not you or I. President Obama made it clear when he was debating Mitt Romney that any individual or married couple making over $200,000/$250,000 is considered rich, and will be targeted for increased taxes and deduction/credit phaseouts. The compromise in the House was made for increasing taxes on income over $413,200 a year.

Now, Joe Bide says he plans to raise taxes on anybody making over $400,000 a year. That's much more reasonable than the $200,000/$250,000, especially due to inflation and residents in higher cost of living areas.

The above chart highlights five different scenarios that encapsulates most people. The first two scenarios in blue are for people who are employees only. Most people don't take full advantage of their pre-tax retirement contributions (scenario 1), but some people do (scenario 2) and will really accumulate a health financial nut over time.

The three other scenarios in red are employee plus contractor scenarios, which enables one to save way beyond the typical amounts due to the opening of a SEP-IRA or Solo 401k as a contractor, whichever your employer doesn't have.

Here are the five hurdles one must overcome to get into scenarios 3-5:

1) Your employer might not agree to let you start your own business or work as an independent contractor. The solution is to join a company that provides you the flexibility to consult after hours. Maybe you become an employee of a relative, a good friend, or simply a progressive company that allows for greater freedom.

2) Your employer might not value you enough to pay you $212,000+ in salary.

3) Even if your employer pays you a $212,000+ salary, they might not be willing to then provide profit sharing up to the maximum limit a year via a SEP-IRA or 401k plan. It is more common for larger corporations to offer 401ks over SEP-IRAs because once a business says they will contribute X % to an employee's SEP-IRA, they have to contribute X % to all employee's SEP-IRA. You can see how the cost to the business can get very cumbersome. With a 401k plan, a company allows the employee to choose their own contribution, and then offer usually a much smaller employee match.

4) You must not have common ownership in any of the employers you work for. As soon as you have common ownership because you started the company or you and your wife started the company, the IRS has new limitations of contribution for you. The IRS doesn't want you to open up 10 different companies, spread out your millions in income, and defer $550,000 ($55,000 X10) in tax free earnings in your retirement.

5) You've got to remove your limiting beliefs about how much you can make as a sole proprietor. If you think making $220,000+ as an employee is difficult, wait until you try making $220,000+ with your own two hands from nothing! But like anything that is done over a long enough period of time, things get better due to experience, expertise, and higher rates.

Come retirement time, we'll still have to pay taxes on all our pre-tax contributions when it's time to withdraw funds. By then, we'll surely be able to tactfully withdraw money in a way that gets taxed the least. Chances are higher that when we're in our 60s, 70s, 80s, and beyond, we won't be making as much money as when we were working anyway.

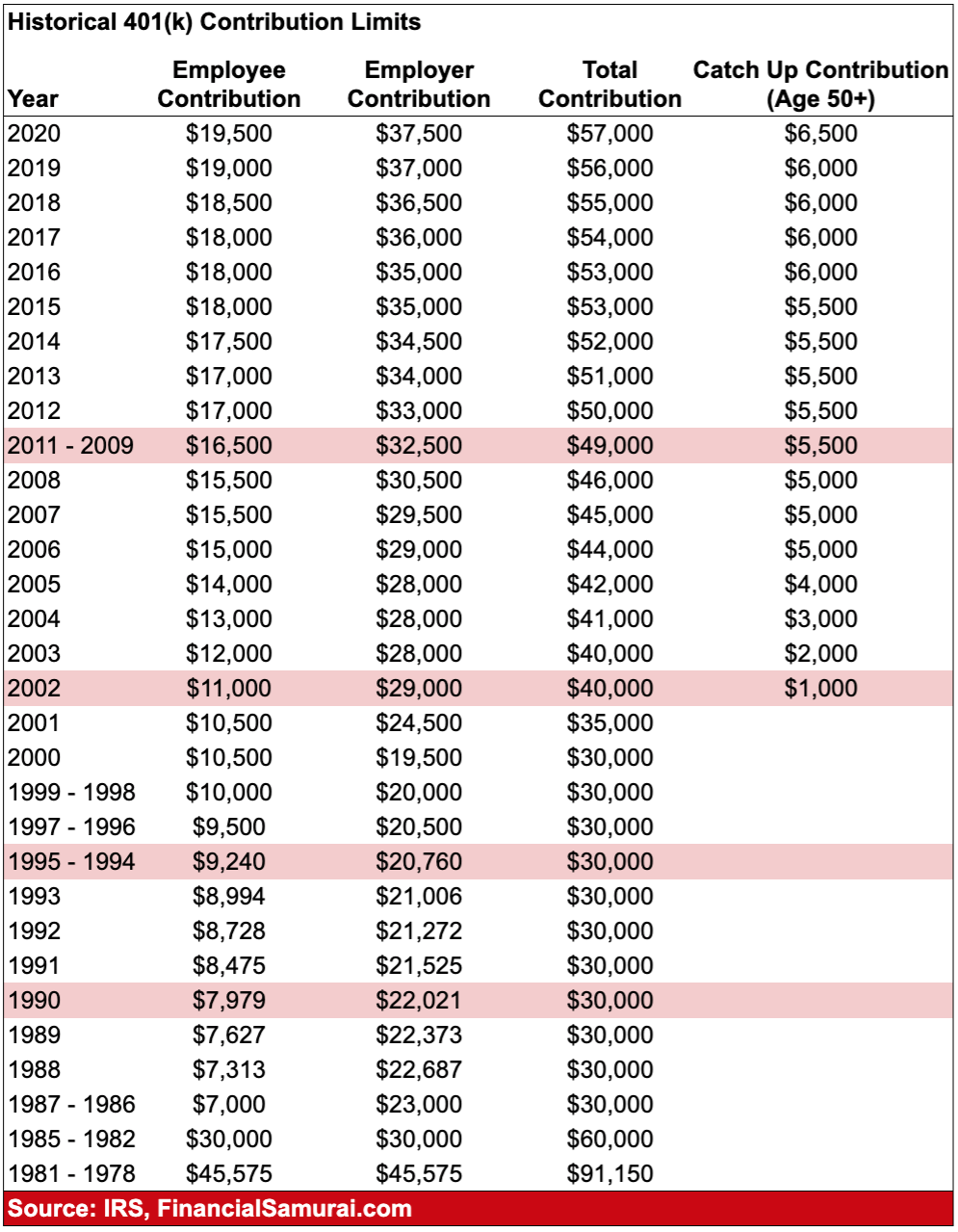

Historical 401k Contribution Limits

2021 401k limit contribution is the same as 2020. Hopefully the 401(k) maximum contribution limit goes up to $20,000 in 2022.

Note: I'm not a tax accountant. It's always worth speaking to a tax advisor about such things. 1099 income for an independent contractor/sole proprietor is tricky and you would have to make closer to ~$260,000 income to get to max out at $56,000 (for 2019) due to taxes and adjustments for a SEP-IRA.

The biggest confusion people have is thinking $56,000 is the limit across all accounts. I thought the same thing too. $56,000 for 2019 is the maximum you, the individual/sole proprietor/owner of your business can contribute. But if you are somehow an amazing person who can get employers to hire you, pay you lots of money, and contribute the max $56,000 a year, then it's the individual company's choice to contribute to your retirement up to the maximum if they wish. It helps to think like an employer when it comes to such dynamics.

Diversify Your Investments Into Real Estate

Stocks are very volatile compared to real estate. Therefore, if you want to dampen volatility and build wealth at the same time, invest in real estate. Real estate is my favorite asset class to build wealth.

The combination of rising rents and rising capital values is a very powerful wealth-builder. Further, investing in real estate is very tax efficient. Depreciation is a non-cash expense that lowers your taxable rental income. Further, you get to sell a property $250,000/$500,000 tax-free if you live in it two out of your last five years!

In 2016, I started diversifying into heartland real estate to take advantage of lower valuations and higher cap rates. I did so by investing $810,000 with real estate crowdfunding platforms. With interest rates down, the value of cash flow is up. Further, the pandemic has made working from home more common.

Take a look at my two favorite real estate crowdfunding platforms. Both are free to sign up and explore.

Fundrise: A way for accredited and non-accredited investors to diversify into real estate through private eFunds. Fundrise has been around since 2012 and has consistently generated steady returns, no matter what the stock market is doing. For most people, investing in a diversified eREIT is the easiest way to gain real estate exposure.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations, higher rental yields, and potentially higher growth due to job growth and demographic trends. If you have a lot more capital, you can build you own diversified real estate portfolio.

I recommend signing up for Personal Capital, the best free financial management tool online. It helps you track your net worth, analyze your investments for excessive fees, and manage your cash flow. I ran my 401k through their 401k Fee Analyzer and found out I was paying $1,700 a year in fees I had no idea I was paying!

Personal Capital has an incredible Retirement Planning Calculator that uses your linked accounts to run a Monte Carlo simulation to figure out your financial future. You can input various income and expense variables to see the outcomes.

Can You Roll a 401k Into Sep Ira

Source: https://www.financialsamurai.com/how-to-save-more-than-100000-a-year-pre-tax-open-a-sep-ira-or-solo-401k/

Belum ada Komentar untuk "Can You Roll a 401k Into Sep Ira"

Posting Komentar